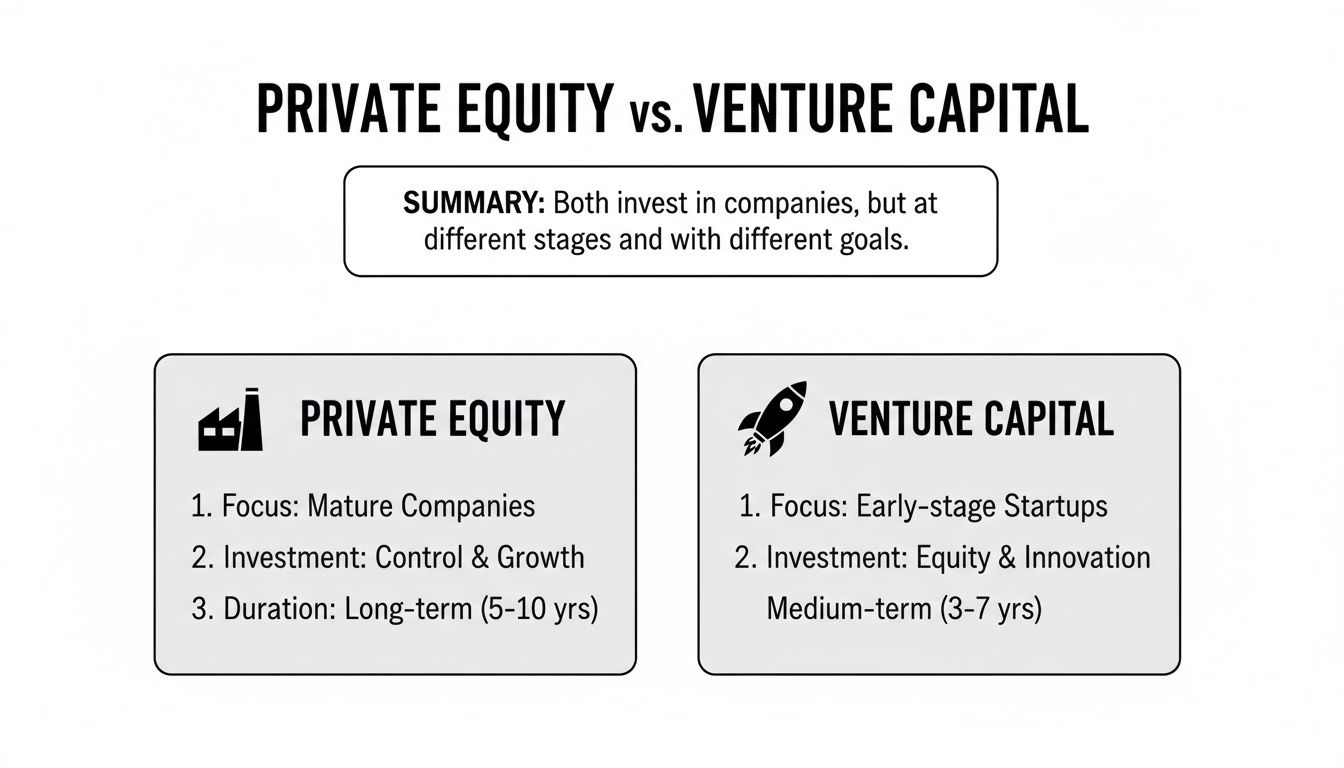

When you boil it down, the core difference in the private equity vs venture capital discussion is pretty straightforward. Private equity (PE) buys mature companies, while venture capital (VC) funds high-growth startups.

PE firms typically acquire a controlling interest in an established business, often using a significant amount of debt to make it happen. Their game plan is to improve operations and whip the company's financials into shape. VCs, on the other hand, take a completely different tack. They invest in early-stage companies for a minority stake, fully accepting the high risk in exchange for a shot at exponential returns if a company truly takes off.

Understanding Private Equity vs Venture Capital At A Glance

While both PE and VC are players in the alternative assets space, they operate in different worlds. Their investment targets, risk tolerance, and playbooks for creating value couldn't be more distinct. Getting these differences is critical, whether you're a founder looking for cash, an LP deciding where to put your money, or a finance professional carving out a career path.

The main split comes down to the maturity of the target company. Private equity is all about stability—businesses with predictable cash flow, a solid market position, and clear opportunities for operational fixes. Venture capital thrives on the exact opposite: instability and disruption. They're chasing new technologies, unproven business models, and markets just waiting to be turned upside down.

This infographic breaks down the two approaches perfectly, showing PE’s focus on established players versus VC’s bet on the future.

As you can see, PE firms act more like strategic operators taking the wheel, while VCs are the capital partners fueling a startup's long and often bumpy ride. These fundamental differences ripple through everything, from the size of the check they write to how hands-on they are with their portfolio companies. If you're curious about the investors who back these funds, you can learn more about the thousands of limited partners investing in VC and PE.

To put it all in one place, here’s a quick summary of the most important distinctions.

Key Differences: Private Equity vs Venture Capital

Ultimately, this table highlights how PE is a game of optimization and control, whereas VC is a high-stakes bet on innovation and scale.

Comparing Investment Philosophies and Deal Structures

At the heart of the private equity versus venture capital debate are two completely different mindsets. These philosophies shape everything—from the companies they target to how they structure deals and ultimately, how they make money. Think of private equity firms as strategic operators, not just passive investors.

Their main objective is to take control of a mature, stable business and make it run better. This control-first approach is perfectly captured by their signature move: the leveraged buyout (LBO). In an LBO, the PE firm borrows a substantial amount of money to buy the company, using the target's own assets and cash flow as security for the loan.

Once they’re in the driver's seat, the firm gets to work. They focus on financial engineering—like restructuring debt or tightening up working capital—and pushing through operational improvements to boost profits and cash flow.

The Private Equity Playbook in Action

Imagine a well-known consumer brand that's lost its edge. A PE firm might see an opportunity and acquire it with a clear game plan:

- Slash operational costs by retooling the supply chain.

- Push into new geographic markets to kickstart revenue growth.

- Sell off non-essential business units to simplify operations and pay down debt.

It’s a hands-on, methodical process. The goal isn't to invent something from scratch but to unlock the hidden potential within an existing business over a multi-year hold.

Venture capital, on the other hand, plays a totally different game. VCs are growth partners, not turnaround artists. They place bets on unproven, early-stage startups that have the potential to disrupt entire industries, fully aware that most of these bets won't pay off.

Venture capital is a game of home runs. The entire model hinges on the belief that one or two massive successes—finding the next Google or Airbnb—will deliver returns so large they eclipse all the losses from the rest of the portfolio.

The Venture Capital Growth Partnership

VCs invest capital and offer strategic advice in return for a minority stake. They rarely want to run the company; they’re backing the founders' vision and their ability to execute. Deals are structured in stages—Seed, Series A, Series B, and so on—with new funding unlocked as the startup hits critical milestones.

For example, a seed-stage tech company gets a small check to build its first product and prove people want it. If they succeed, they can raise a much larger Series A round to pour fuel on the fire and scale up their sales and marketing. This step-by-step funding helps VCs manage their risk while giving the startup the cash it needs to grow explosively.

The VC's job is to be a mentor and a connector. They open up their network to help the founders find talent, customers, and the next round of investors. It’s a high-risk gamble on innovation and market creation—a world away from the PE model of operational control and predictable value enhancement.

How the Money Works: A Look at Fund Mechanics and Capital

The machinery behind private equity and venture capital funds is worlds apart, and it all starts with the size of the checks they write and where that money comes from. PE deals are massive undertakings, frequently running into the hundreds of millions or even billions, because they're buying entire, established companies. We've seen the average PE deal size nearly double since 2023, pointing to a market doing fewer but much bigger transactions.

Venture capital, on the other hand, plays a completely different game. The deals are smaller and intentionally staggered. A startup might raise a $1 million seed round to get off the ground, then a $10 million Series A to scale, and maybe a $50 million Series B to go for market leadership. This step-by-step funding lets VCs manage their risk, releasing more cash only after the startup proves itself by hitting critical milestones.

This massive difference in deal size is a direct result of how they finance their investments. When you break it down, the private equity vs. venture capital comparison gets crystal clear.

Debt Leverage vs. Equity Partnership

Private equity firms are wizards of financial engineering, and their main tool is debt. The classic leveraged buyout (LBO) is built on borrowing heavily from debt markets to fund an acquisition. By using leverage, a PE fund can take control of a huge company with a surprisingly small slice of its own equity, amplifying potential returns. This strategy only works because their targets are mature businesses with predictable cash flows solid enough to handle the debt payments.

Venture capital is almost exclusively an equity game. VCs invest capital from their limited partners directly into a startup, getting company shares in return. You won't see a VC loading up a young, cash-burning startup with debt. Instead, they become true equity partners, sharing the immense risk for a shot at an equally immense upside. For a deeper dive into how VCs vet these risky bets, this venture capital due diligence checklist breaks down their rigorous process.

The simplest way to think about it is this: PE uses other people's money (debt) to buy companies, while VC uses its partners' money (equity) to build them. This one difference dictates almost everything else, from risk tolerance to how they make money.

A Tale of Two Timelines

On paper, both PE and VC funds look similar, typically running on a 10-year lifecycle with a possible two-year extension (the classic "10+2" model). But how they spend that decade is completely different, a reflection of how long it takes their portfolio companies to grow up.

- Investment Period: A PE fund gets to work fast. Its investment period is usually a concentrated 3-5 years. The goal is to acquire all their target companies quickly so they can roll up their sleeves and start executing their value-creation playbook.

- Harvesting Period: VCs need more patience. They might deploy capital over a longer 5-7 year window, following on as their startups climb from one funding round to the next. This naturally pushes their "harvesting" or exit period much later into the fund's life. It can easily take a decade or more before a startup is mature enough for a big exit through an IPO or acquisition.

Evaluating Return Profiles and Risk Metrics

When you peel back the layers, private equity and venture capital are playing entirely different games when it comes to risk and return. They might operate in the same private markets, but their financial philosophies couldn't be more distinct.

Private equity is engineered for stability and predictable growth. PE firms hunt for established, mature companies where they can apply proven operational and financial strategies to unlock value. The goal is to generate steady, reliable returns, often targeting a 2-3x Multiple on Invested Capital (MoIC).

This whole approach is built on minimizing risk. By securing a controlling stake, PE managers can directly implement changes, streamline operations, and use disciplined financial management to pay down the debt from the buyout. They’re essentially building a better, more profitable version of an already-successful business.

The Power Law of Venture Capital Returns

Venture capital, on the other hand, thrives on a financial principle known as the power-law distribution. This is a high-stakes model where VCs go in fully expecting most of their portfolio companies to fail or barely break even. The entire fund's performance is pinned on just one or two massive wins.

These are the "home run" investments that deliver outlier returns—we're talking 10x, 50x, or even 100x the initial capital. It’s a game of embracing extreme uncertainty, where a single blockbuster exit can pay for all the losses and still return the entire fund multiple times over. Managing this kind of portfolio isn't for the faint of heart; it requires a sophisticated understanding of risk, as detailed in how VCs use data to manage portfolio risk.

VC is a game of outliers. Success isn't measured by the average return of the portfolio companies, but by the massive success of the one or two that redefine a market and deliver exponential growth.

Key Metrics for Performance Evaluation

While both PE and VC funds report performance to their Limited Partners (LPs) using similar metrics, the story behind the numbers is completely different. At the heart of it all is the ability to understand how to value companies, a critical skill for any investor in these asset classes.

- Internal Rate of Return (IRR): This metric shows the annualized return on an investment. For PE funds, the IRR tends to be smoother and more consistent as value is steadily created over the holding period. In VC, IRR can be wildly volatile, especially in a fund's early years, because it can be skewed dramatically by the timing of a single large exit.

- Multiple on Invested Capital (MoIC): Also called TVPI (Total Value to Paid-In Capital), this simply shows how many times the fund has returned its investors' money. A 2.5x MoIC is considered a solid performance in private equity. For a VC fund, the bar is much higher—it often needs to hit 3x or more just to be considered successful, thanks to the high loss rate.

Let's look at the return profiles and risk expectations side-by-side to make the differences crystal clear.

Return Profile and Risk Comparison

As the table shows, a PE fund's success is judged on its ability to consistently deliver solid multiples across its portfolio, while a VC fund is defined by its ability to find and back a generation-defining company.

Historically, private equity has been a strong performer. One comprehensive study tracking state pension allocations over a 23-year period found that PE delivered an 11.0% net-of-fees annualized return. This handily beat the public stock benchmark's 6.2% over the same timeframe.

Navigating Governance Control and Exit Strategies

Once a deal closes, the relationship between a fund and its portfolio company shifts into a new phase. This is where the differences between private equity and venture capital really come into focus. Governance and control aren't just legal terms on a page; they dictate the entire post-investment partnership and ultimately shape how everyone gets their money back.

Private equity firms operate from a position of control. By taking a majority ownership stake, they’ve earned the right to steer the ship. This is far from passive ownership. PE investors often take an active, hands-on role, sometimes bringing in a new CEO, appointing new board members, and directly pushing for strategic changes designed to maximize the company's value for an eventual sale.

Holding the reins gives PE firms a lot of say over the exit strategy. They can meticulously time and manage the exit to hit their return targets. The most common exit routes for PE include:

- Strategic Sale: Selling the business to a larger corporation, often a direct competitor or a company in an adjacent market.

- Secondary Buyout: Selling the company to another private equity firm that sees a new angle for value creation.

- Initial Public Offering (IPO): Taking the company public, which is a viable but less frequent option compared to a sale.

The VC Approach to Guidance and Exits

Venture capital firms, on the other hand, hold a minority stake and play a completely different game. They act more like influential guides than day-to-day operators. A VC partner will usually take a board seat, offering mentorship, strategic advice, and, most importantly, access to their network of talent, customers, and potential future investors. But they don't have the direct operational control of a PE owner.

This founder-investor dynamic is built on collaboration, with the VC backing the founding team's vision. Managing these relationships effectively is a core part of the broader conversation on the state of digitalization in private equity and venture capital, as modern platforms become essential for communication and data sharing.

For venture capital, the exit is the entire point of the investment. A VC-backed startup isn't built to generate steady dividends; it's built to be sold or go public, delivering the massive home-run return their limited partners expect.

For a successful startup, the typical exit is an acquisition by a major tech company or a headline-grabbing IPO. These are the kinds of events that deliver the exponential returns needed to make up for the fund’s many losses. The VC model is famous for its extreme return dispersion—a small handful of companies, maybe just 10–15%, generate the vast majority of the fund's returns. Meanwhile, nearly half of all startups fail to even return the capital invested.

This high-risk, high-reward dynamic is precisely why VCs push their winning companies toward enormous exits. It’s the only way the fund's math works.

Choosing the Right Capital For Your Situation

Deciding between private equity and venture capital isn't just a technicality—it's a fundamental choice that depends entirely on your goals. Whether you’re a founder looking to scale or a Limited Partner building a portfolio, the right answer comes down to your company's stage, your tolerance for risk, and where you want to be in the long run.

For business owners, the paths are quite distinct. Private equity is the go-to for established, profitable companies at a crossroads. Think of a multi-generational manufacturing firm looking for a smooth succession or a solid software business that needs a capital injection and operational guidance to expand globally. These are businesses with proven playbooks, not moonshots.

Venture capital, on the other hand, thrives on disruption. It's the fuel for a pre-revenue tech startup with a brilliant, unproven idea. Founders who go the VC route need to be comfortable trading a hefty equity stake for the chance at explosive growth and market domination, prioritizing scale over short-term profits.

Guidance for Limited Partners

For LPs, the private equity vs. venture capital debate is all about strategic portfolio construction. You're balancing risk and reward to hit your return targets, and each asset class plays a very different role.

A smart institutional portfolio often has a place for both. Private equity acts as the steady foundation, delivering predictable returns, while a calculated allocation to venture capital provides the high-octane potential for those massive wins that can elevate the entire portfolio's performance.

This is where a portfolio intelligence platform like Vestberry becomes indispensable. It gives LPs a unified view to track their diverse holdings in one place.

With a clear dashboard, investors can monitor everything from high-level portfolio value down to the nitty-gritty metrics of each fund. This kind of transparency is crucial for managing the distinct risk profiles of PE and VC.

Ultimately, LPs can build a portfolio that maps to their specific goals:

- Private Equity: Use it for stable, long-term growth and downside protection. It’s your source for generating predictable cash flow.

- Venture Capital: Allocate here for high-growth potential. You're accepting higher risk and longer timelines in exchange for the shot at exceptional, fund-returning gains.

Answering Your Lingering Questions

Even after breaking down the differences, some practical questions about private equity and venture capital tend to pop up. Let's tackle a few of the most common ones to really solidify the concepts.

Why Do PE Deals Involve So Much Debt?

The heavy use of debt in private equity, especially in a leveraged buyout (LBO), boils down to one simple goal: boosting returns. When a PE firm uses borrowed money for a huge chunk of the purchase price, it dramatically reduces how much of its own cash it has to put in.

This financial engineering acts like a lever, magnifying the potential upside when they eventually sell the company. It's a strategy that only works because PE targets are mature businesses with predictable, steady cash flows—the very cash flows needed to make the hefty debt payments after the deal closes. Essentially, the company they buy is strong enough to pay for its own acquisition.

Why Do VCs Invest in Stages?

Venture capital funding is delivered in stages (think Seed, Series A, Series B, etc.) as a way to manage the massive risk inherent in backing startups. An early-stage company is unproven, so VCs release capital in smaller, incremental chunks tied to hitting specific milestones.

These milestones might be anything from finishing a prototype or signing the first major customer to reaching a certain revenue run rate.

This milestone-based funding keeps everyone honest. It protects the investor's capital and ensures the founders stay laser-focused on proving their model before getting the big checks needed for full-scale growth.

Which Is Riskier: Private Equity or Venture Capital?

Without a doubt, venture capital is the riskier of the two. The entire VC model accepts that most portfolio companies will fail. A fund’s success hinges on just one or two massive wins—the "home runs"—that deliver outlier returns of 10x or more, more than making up for all the other losses.

Private equity, on the other hand, is built on a foundation of lower risk. PE firms buy established companies that already have a working business model and real cash flow. Their game is not about betting on a radical new idea; it’s about making smart operational improvements and financial adjustments to grind out more predictable, stable returns.

Turn your complex fund data into a strategic advantage. Vestberry offers a single source of truth for portfolio intelligence, helping you make faster, data-backed decisions and streamline LP reporting. See how Vestberry can support your firm.