Valuing a private company isn't just about crunching numbers; it's about piecing together a puzzle without a picture on the box. It involves a mix of rigorous financial analysis, like Discounted Cash Flow (DCF) or market multiples, and careful adjustments for things like illiquidity. The goal is to land on a defensible estimate of worth, a figure that can guide investment decisions, satisfy stakeholders, and stand up to scrutiny during a transaction.

Why Private Company Valuation Is More Art Than Science

There’s a world of difference between valuing a public company and a private one. Public companies have a stock ticker flashing a new price every second—a constant, market-driven verdict on their value. Private companies? They operate without that real-time feedback loop. This lack of a clear, public price is exactly why a structured private company valuation process is so critical for founders, investors, and fund managers alike.

Think of it like appraising a one-of-a-kind painting. An appraiser will look at the artist's reputation, the materials used, and the painting's condition. That’s the objective side of things, much like digging into a company's financial statements. And before you can even think about complex valuation models, it’s essential to nail the basics by understanding the difference between P&L and Balance Sheet.

But the appraiser doesn't stop there. They also consider what similar works have sold for recently and what the current appetite is for that style of art. This is the market context—the subjective, forward-looking part of the equation.

The importance of this process can't be overstated. It's a fundamental part of managing private market investments, especially for Venture Capital (VC) and Private Equity (PE) firms.

Let's look at the main reasons why this discipline is so crucial.

Why Private Company Valuation Matters

As you can see, a solid valuation underpins nearly every major financial event in a private company's lifecycle, ensuring that decisions are based on sound analysis rather than guesswork.

A Strategic Tool, Not a Compliance Chore

At its best, valuation is a strategic tool, not just a box-ticking exercise for auditors. For VC and PE firms, conducting regular, thoughtful valuations is essential for:

- Tracking portfolio health: Consistent valuations paint a clear picture of how your investments are actually performing over time, beyond just cash-on-cash returns.

- Guiding investment decisions: A solid valuation helps you set an entry price for a new deal and, just as importantly, informs your strategy for follow-on funding rounds.

- Communicating value to Limited Partners (LPs): Nothing builds trust with LPs like transparent, well-documented valuations that clearly explain the "why" behind the numbers.

The private markets have grown up. The days of back-of-the-napkin valuations are long gone. The explosion of unicorn companies tells the story best: as of April 2025, over 1,200 unicorns were collectively valued at more than $4.3 trillion. That’s a staggering 20x jump from just $300 billion in 2013, a surge driven by a flood of venture capital and massive technological shifts. By the end of the year, projections pushed that total to over $5.9 trillion, a testament to the immense value being created outside of the public markets.

A robust valuation serves as a navigational chart for investors. It grounds strategic decisions in defensible data, transforming abstract potential into a quantifiable measure of worth that can be tracked, managed, and ultimately realized.

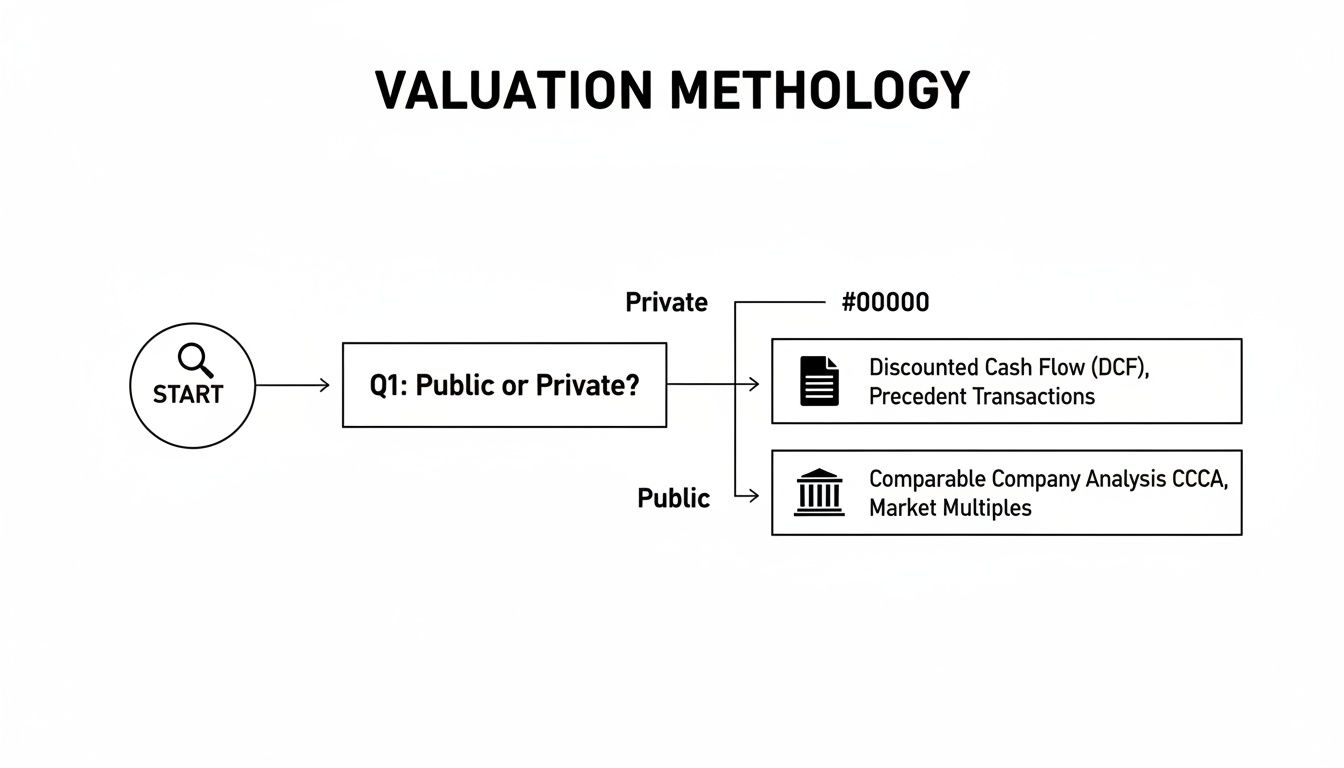

Choosing the Right Valuation Method

Picking the right valuation method for a private company is a lot like a carpenter choosing the right tool. You wouldn't use a sledgehammer to drive a finishing nail, and you wouldn't use a delicate financial model on a pre-revenue startup. The right approach depends entirely on the company's stage, its industry, and the quality of the data you can get your hands on.

There are three primary toolkits every practitioner needs to master. Each gives you a different lens to view a company's worth. The real art of a defensible private company valuation isn’t about sticking rigidly to one method; it's about knowing which one to lean on and how to use the others as a reality check.

This decision tree helps visualize how to start thinking about the process.

As you can see, public company valuations often lean heavily on market multiples. For private companies, we need a broader toolkit that blends internal forecasts (like a DCF) with signals from the outside world (like precedent transactions).

The Income Approach: Forecasting Future Earnings

The Income Approach is all about a company's ability to generate cash in the future. The most common tool here is the Discounted Cash Flow (DCF) analysis.

Think of it like buying an apartment building. You're not just buying bricks and mortar; you're buying the stream of rental income it will produce over the next 20 years. A DCF model does something very similar for a business—it projects future cash flows and then "discounts" them back to what they’re worth today. After all, a dollar you might earn in ten years is worth less than a dollar in your pocket right now.

This method is the gold standard for mature, stable businesses with a predictable track record. Its biggest strength is that it’s based on the company’s fundamental performance, not just the whims of the market.

The core idea behind the Income Approach is that a business's value today is the sum of all its future cash flows, adjusted for risk and the time value of money. It asks one simple question: "What is this company's future earning power worth right now?"

The Market Approach: Looking at the Neighbors

The Market Approach is probably the most intuitive. It values a company by looking at what similar businesses are worth. It’s exactly like pricing your house by checking what comparable homes on your street have sold for recently.

You have two main ways to do this:

- Comparable Company Analysis (CCA): This involves looking at valuation multiples (like EV/Revenue or EV/EBITDA) of publicly traded companies in the same industry with a similar growth profile. For private SaaS companies, for instance, the median public market multiple was around 7.0x run-rate revenue at the start of 2025.

- Precedent Transactions: Here, you analyze the prices paid in recent mergers and acquisitions of similar private companies. This is often the most direct evidence of market value because it shows what a real buyer was actually willing to pay for a comparable asset.

The Market Approach is incredibly helpful for companies in established industries with plenty of public comps. It’s also the go-to for early-stage startups where a recent funding round essentially sets the "market price" for the company's shares.

The Asset-Based Approach: Summing Up the Parts

Last, we have the Asset-Based Approach. This method values a company based on the total value of its assets minus its liabilities. It’s like valuing a car by adding up the price of its engine, tires, and frame instead of what someone would pay for the whole running vehicle.

For growing, profitable businesses, this method is less common. Why? Because it completely ignores intangible assets like brand reputation, customer lists, and future growth potential—which are often the most valuable parts of a modern company.

But it has its moments and becomes highly relevant in a few key situations:

- For holding companies with significant tangible assets, like real estate or heavy machinery.

- In liquidation scenarios, where the business is literally worth more "dead than alive."

- For very early-stage startups that have yet to generate revenue, as their value is mostly tied to the assets they've built so far.

At the end of the day, a truly robust valuation rarely relies on a single method. A good analyst will build a detailed DCF model and then sanity-check that result against market multiples from recent deals. This triangulation gives you a much more complete—and defensible—picture of what a company is truly worth.

To help you navigate these choices, here's a quick cheat sheet for deciding which method is best for your situation.

How to Choose Your Valuation Method

Each method provides a different piece of the puzzle. Using them in combination is where the real skill lies, helping you build a valuation that is not just a number, but a well-reasoned argument.

Applying Crucial Adjustments to Your Valuation

Running a DCF or pulling comps gets you a preliminary number, but that's just the starting line. A raw calculation doesn't capture the real-world experience of owning a piece of a private business. This is where you have to apply some crucial adjustments to turn a theoretical value into a defensible one.

These aren’t just minor tweaks. They’re fundamental acknowledgments of what makes private equity different from public stock. The two most important concepts every investor and appraiser needs to master are the Discount for Lack of Marketability (DLOM) and the adjustments for control.

The Illiquidity Factor and DLOM

Think about it. If you own shares in Apple, you can liquidate them in seconds with a few clicks. But what if you own a stake in a local software startup? Selling those shares is a whole different ballgame. You have to find a buyer, negotiate a price, and navigate transfer restrictions. It's a process.

That difference in liquidity has a real, tangible impact on value. The Discount for Lack of Marketability (DLOM) is exactly what it sounds like: a discount you apply because an ownership stake in a private company is much harder to sell than a public one. Any rational investor is going to pay less for an asset they can't easily turn back into cash.

It's like selling a highly customized sports car versus a brand-new Toyota Camry. The Camry has a massive, active market, and you can sell it quickly at a predictable price. The custom car might be incredible, but finding that one specific buyer who values its unique features will take time and effort. If you need to sell it fast, you’ll probably have to offer a discount.

Putting a number on DLOM is a nuanced exercise, often involving complex models that weigh things like expected holding periods and company volatility. But it's an absolutely essential step for arriving at a fair value that can withstand an audit. These discounts aren't trivial, either—they often range from 10% to 30%, and sometimes even more, depending on the company's situation.

Control Premiums and Minority Discounts

Even within the same company, not all shares are created equal. The amount of influence your ownership stake carries dramatically changes its per-share value. This brings us to control premiums and their flip side, discounts for lack of control (DLOC).

A control premium is the extra amount an acquirer is willing to pay to gain a controlling interest in a company. Owning more than 50% of the voting shares isn't just about getting a bigger slice of the pie; it’s about controlling the entire recipe.

A controlling shareholder gets to:

- Hire and fire the management team.

- Set the company's strategic direction.

- Dictate dividend policies.

- Decide whether to sell the company.

The power to steer the ship is incredibly valuable. This is why a 51% stake is worth more on a per-share basis than a 1% stake. The minority shareholder is just along for the ride, with very little say in where the company is headed. For that reason, a Discount for Lack of Control (DLOC) is applied to minority positions.

The size of these premiums and discounts changes based on the industry and the specific deal, but they reflect the undeniable value of being in charge. The mega-valuations we see in private markets often factor in the strategic value a buyer places on controlling a foundational technology.

For example, by late 2025, OpenAI had cemented its position as the world's most valuable private company with an eye-watering $500 billion valuation following a $6.6 billion secondary share sale. That number is a clear signal of the immense strategic premium investors place on controlling a leader in the AI sector. It's a perfect illustration of how control can drive value far beyond simple financial metrics. You can discover more insights about the trends shaping the most valuable private companies in our full report.

Understanding Valuation for Reporting vs. Transactions

One of the most common questions I get from founders and fund managers is why the valuation on a quarterly report looks so different from the price tag in an M&A offer. It's a great question, and the answer is simple: they're calculated for entirely different reasons. The purpose of the valuation dictates everything that follows.

Think of it like this: a reporting valuation is like getting your house appraised for property taxes. The appraiser follows a strict, standardized process to arrive at a defensible, conservative number.

A transaction valuation, on the other hand, is like getting an offer from a buyer who desperately wants to live in your specific neighborhood, loves your backyard, and is willing to pay a premium to close the deal. It’s all about what the asset is worth to one specific buyer at one specific moment.

The Purpose of Reporting Valuations

A reporting valuation is all about creating a consistent, auditable "mark-to-market" value for your portfolio. This is the number your Limited Partners (LPs) and auditors see every quarter. It's often called a Fair Value assessment, guided by accounting standards like ASC 820.

The whole process is designed to be disciplined. It prioritizes:

- Objectivity: Using verifiable data and standard models so an independent party could arrive at a similar conclusion.

- Conservatism: Leaning away from speculative or overly optimistic assumptions to ensure the value is supportable.

- Consistency: Applying the same methods across the portfolio and over time, which allows for true performance tracking.

The final number represents what a hypothetical, impartial buyer might pay—not what a highly motivated strategic acquirer would offer. This rigor is fundamental to maintaining trust and is a huge part of improving LP reporting in venture capital.

A reporting valuation answers the question: "What is a reasonable, supportable value for this asset on our books today, according to established financial principles?"

The Strategic Nature of Transaction Valuations

When a company is actually up for sale, the game changes completely. The valuation stops being a compliance exercise and becomes a strategic, forward-looking negotiation. A buyer isn't just assessing the company as it is; they're calculating what it could become as part of their empire.

This is where the magic word "synergies" enters the conversation. A strategic acquirer is often willing to pay a significant premium based on factors that would never show up in a standard fair value calculation.

A transaction valuation will bake in things like:

- Cost Synergies: How much can the buyer save by eliminating redundant roles or overlapping software licenses?

- Revenue Synergies: Can they cross-sell the acquired company's products to their massive customer base?

- Strategic Value: Does buying this company give them a foothold in a new market, eliminate a competitor, or bring in world-class talent they couldn't hire otherwise?

Because these factors are unique to a specific buyer, the final sale price can—and often does—end up much higher than the last reported fair value. It’s no longer about a hypothetical market; it's about the maximum price a single, motivated buyer is willing to pay to win.

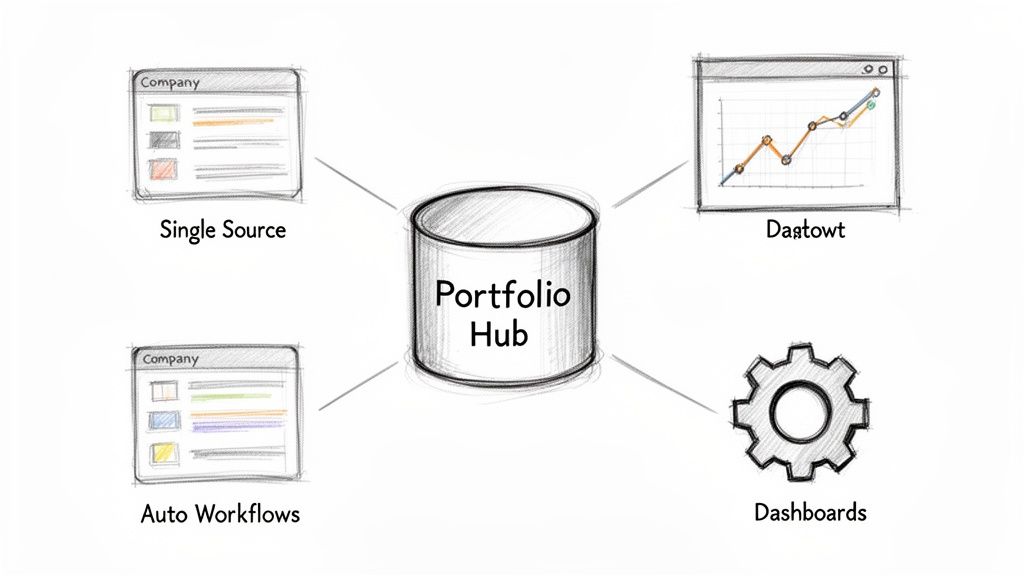

How Portfolio Intelligence Platforms Fix the Valuation Mess

The diagram above isn't just a clean graphic; it's a blueprint for escaping the manual, error-prone processes that still bog down so many private market investors. It shows how a central hub can turn raw data into genuine valuation insights.

Moving from valuation theory to the real world is where things get messy for most VC and PE firms. The reality is often a chaotic maze of disconnected spreadsheets, out-of-date financials from portfolio companies, and hours of painstaking manual data entry. This patchwork of information creates a shaky foundation for any private company valuation model.

When your inputs are unreliable, your outputs become indefensible. Inconsistent data leads to inconsistent valuation methods, making it nearly impossible to track performance accurately, justify fair value marks to LPs, or satisfy auditors. It's a time-consuming, frustrating cycle that pulls your best people away from what they should be doing: sourcing deals and creating value.

The Power of a Single Source of Truth

This is where a modern portfolio intelligence platform completely changes the game. By creating a single source of truth, these systems cut through the chaos of scattered data. Instead of chasing down financials and wrestling with conflicting spreadsheets, fund managers get a centralized database where all portfolio company metrics are standardized and always up to date.

This commitment to clean data has a direct and immediate impact on valuation accuracy.

- Reliable Inputs: Clean, consistent data feeds directly into your valuation models. This ensures that any calculation—whether it's a DCF, market multiple, or another method—is based on the most current and accurate information possible.

- Methodology Consistency: Automated workflows make sure your firm's valuation policies are applied the same way across every asset, every single quarter. This takes human error and subjective bias out of the equation.

- Dynamic Monitoring: Live dashboards let you see how fair value is changing as new data rolls in. You get a dynamic view of portfolio health, not just a static snapshot once a quarter.

A portfolio intelligence platform turns valuation from a reactive, manual chore into a proactive, data-driven discipline. It provides the core infrastructure you need to build institutional credibility and operational excellence.

From Data Wrangling to Value Creation

Bringing in a dedicated platform is more than an efficiency play; it's a strategic shift. Think about it: when your team is no longer burning dozens of hours each quarter just to pull together valuation reports, where does that time go? It goes toward analyzing performance, supporting portfolio companies, and hunting for the next great investment.

In 2025, the global private equity and venture capital space saw deal value jump 42.57% year-over-year to an incredible $468.51 billion. For GPs still juggling fragmented data, that number should be a wake-up call. As deal volumes rise, teams risk drowning in spreadsheets while competitors are using powerful portfolio management software to make faster, data-backed decisions. You can read the full research on the 2025 private equity deal surge from S&P Global.

Ultimately, these platforms help funds get in line with industry best practices, including ILPA guidelines for transparency. By giving LPs clear, consistent, and well-documented valuations, you build the kind of trust that's essential for long-term success in the private markets.

Establishing a Defensible Valuation Process

A calculated number is just a number. A defensible private company valuation, on the other hand, is a rigorous, well-documented process that can withstand intense scrutiny from auditors, regulators, and your own LPs. Moving from a simple calculation to an institutionalized process is what separates the mature fund managers from the pack.

It’s not enough to just run a model. You have to be able to show your work, justify every assumption, and prove that your approach is both consistent and objective. This turns valuation from a quarterly chore into a core pillar of your firm’s credibility. Think of it like building a case for a jury—the verdict hinges on the quality of your evidence and the clarity of your argument.

Building Your Governance Framework

The cornerstone of any defensible process is a formal valuation policy. This document is your firm’s constitution for valuation. It should clearly outline the methodologies you use, how you select key inputs, and the frequency of your reviews, ensuring everyone on your team is playing from the same sheet of music.

Within this framework, creating a dedicated valuation committee is a game-changer. This group, typically made up of senior partners and finance professionals, provides essential oversight and challenges the assumptions made by the deal team. Their involvement adds a critical layer of independent review, which goes a long way in proving the objectivity of your final fair value mark.

A defensible valuation is built on process, not perfection. An auditor will focus less on whether your valuation was "right" in hindsight and more on whether your process for arriving at that value was reasonable, well-documented, and consistently applied.

The Indispensable Audit Trail

Your ability to defend a valuation comes down to one thing: a meticulous audit trail. This isn't just about saving your final spreadsheet. It’s about documenting the entire journey. Every assumption, every data point, and every decision needs to be recorded and traceable.

A complete audit trail should always include:

- The Valuation Model: The actual spreadsheet or software output showing all calculations.

- Key Assumptions and Inputs: A clear record of the discount rates, growth projections, and market multiples you used, along with the rationale for why you chose them.

- Supporting Market Data: Any third-party reports, comparable company data, or transaction details that informed your model.

- Committee Review Records: Minutes from valuation committee meetings that show discussion points, challenges, and the final approval of the fair value.

To create a truly bulletproof process, robust financial analysis and clear data presentation are non-negotiable. Investing in your team's toolkit by enhancing financial analysis for a defensible valuation process with tools that complement traditional spreadsheets can seriously strengthen your approach.

And of course, streamlining how all this data is collected and presented is crucial. You can see how to move beyond basic Excel reporting to build a system that auditors and LPs will trust. This kind of systematic documentation isn't just a nice-to-have; it's essential for proving your process is built on a foundation of rigor and transparency.

Answering Common Private Company Valuation Questions

Putting theory into practice always brings up questions. When you're in the trenches valuing a private company, the real-world nuances matter. Here are some of the most common questions we hear from VC and PE professionals, with straightforward answers to help guide your process.

How Often Should We Value Our Portfolio?

For most funds, a quarterly portfolio valuation is the gold standard. This rhythm keeps you in sync with Limited Partner (LP) reporting cycles and financial standards like ASC 820. It's about creating a consistent, regular pulse check on your fund's health.

But don't just rely on the calendar. You should trigger a new valuation anytime there's a significant event. This could be anything from a new financing round to a major shift in public market multiples, a big miss on performance targets, or even an unexpected offer to buy the company.

How Does a 409A Valuation Differ from Fair Value?

This is a classic source of confusion, and it's easy to see why. While they use similar techniques, their goals are completely different.

Think of a 409A valuation as a tool specifically for tax compliance in the U.S. Its job is to figure out the fair market value (FMV) of a company's common stock, which is then used to set the strike price for employee stock options.

A Fair Value assessment (under ASC 820) is all about financial reporting. Its purpose is to determine the value of the specific security your fund actually holds—which is often preferred stock—so you can accurately report back to your LPs.

- 409A: For tax compliance on common stock.

- Fair Value: For investor reporting on a fund's specific security.

How Do You Value Pre-Revenue Startups?

Valuing a company with no revenue feels a bit like navigating without a map. Traditional financial models like DCF just don't work when there are no cash flows to discount. It becomes more of an art, focused on potential rather than past performance.

In these situations, investors often turn to a few specialized approaches:

- The Berkus Method: This method assigns a dollar value to key risk factors—like the strength of the management team, the prototype, strategic relationships, and the go-to-market plan.

- The Scorecard Method: Here, you compare the startup to other, similar deals in the region, adjusting its value up or down based on factors like the team, market opportunity, and technology.

- The Venture Capital Method: This approach starts with the end in mind. You project a potential exit value years down the road and then work backward, applying a high discount rate to arrive at today's post-money valuation.

In the real world, the most influential data point for an early-stage company is almost always the valuation set by its last financing round. That post-money figure is the clearest signal you have of what the market thinks it's worth.

What Are the Biggest Mistakes to Avoid?

Even the most experienced investors can stumble. The most expensive mistakes in private company valuation usually boil down to a lack of diligence or consistency.

Watch out for these common traps:

- Relying on a single method. Always pressure-test your primary valuation method with a secondary one to see if your conclusion holds up.

- Using bad comparables. Don't just find companies in the same industry. They need to be truly similar in size, growth profile, and business model.

- Failing to document your assumptions. If you can't explain why you chose a specific multiple or discount rate, your valuation won't stand up in an audit.

- Forgetting key adjustments. Overlooking discounts for lack of marketability (DLOM) or control premiums can lead to a seriously flawed valuation.

- Inconsistent application. Applying your methodologies differently across the portfolio or from one quarter to the next without a good reason is a major red flag for auditors and LPs.

A solid valuation process starts with clean, organized data. Vestberry acts as a single source of truth for VCs and PEs, helping you turn messy portfolio data into the clear insights needed for consistent, auditable, and defensible fair-value calculations. Learn how Vestberry can streamline your valuation workflow.