Private equity fund administrators are the operational engine of a modern PE firm. They take on the complex, time-consuming grind of fund accounting, compliance, and investor reporting. This frees up General Partners (GPs) to do what they do best: focus exclusively on sourcing deals and generating returns.

The Strategic Role of Modern Fund Administrators

Imagine a private equity firm is an elite racing team. The GPs are the star drivers, totally focused on winning the race—which means finding breakout companies and closing high-value deals. In this scenario, the private equity fund administrators are the world-class pit crew and engineering team working tirelessly behind the scenes.

This crew handles everything. They run the engine diagnostics (fund accounting), make sure the car meets every regulation (compliance), and feed performance data back to the team owners (investor reporting). Without them, the drivers would be stuck in the garage with a wrench instead of on the track. This relationship is no longer a simple back-office necessity; it’s a critical part of a winning PE operation.

From Back Office to Strategic Partner

The administrator’s role has completely transformed. A decade ago, they were often viewed as a cost center, a team hired for basic bookkeeping. Today, with funds getting more complex and investors demanding more transparency, they’ve become indispensable strategic partners.

Private markets are huge, with global assets under management hitting €13.2 trillion in 2024. This scale demands a whole new level of operational sophistication. GPs are now under pressure to do far more than just make good deals.

By outsourcing non-investment functions, private equity managers can focus on their core competency—investment management—and potentially improve operational efficiency, reduce costs, and manage risks better.

This shift lets fund managers put all their energy into creating value, knowing that specialists are handling the intricate operational machinery.

Why This Partnership Is Now Critical

So, what’s driving this change? A few key factors have made specialized private equity fund administrators more important than ever. They provide the solid infrastructure needed to compete and build investor trust. A huge part of their value is helping firms to improve operational efficiency and keep things running smoothly.

Here’s why their role is no longer optional:

- Increasing Investor Demands: Limited Partners (LPs) expect a level of transparency that was unheard of years ago. They want detailed, accurate, and timely reports, and administrators deliver the institutional-grade reporting that keeps them confident.

- Regulatory Complexity: The maze of anti-money laundering (AML) rules and other global regulations is constantly changing. Administrators bring dedicated expertise to navigate this, protecting the fund from major financial and reputational risks.

- Technological Advancement: The best administrators use powerful platforms to manage data and automate workflows. When this tech is integrated with a firm’s own systems, like a solid portfolio management software, it creates a powerful and seamless data ecosystem.

In the end, bringing on a fund administrator isn't a luxury anymore. It’s a foundational decision that builds credibility, drives efficiency, and gives a firm the confidence to scale.

What Private Equity Fund Administrators Actually Do

The term "administrator" can be a bit misleading, conjuring images of simple clerical work. In reality, private equity fund administrators are highly specialized operational partners who manage the entire non-investment side of a fund's life.

Think of them as the fund's central nervous system. They handle the complex, mission-critical functions that allow the fund to operate smoothly, from its financial health to its regulatory standing. By taking on these demanding back-office tasks, they free up General Partners (GPs) to do what they do best: find great investments and generate returns.

Fund Accounting and Valuation Support

At the very core of their role is fund accounting, but this is a far cry from basic bookkeeping. It’s the meticulous financial stewardship of the entire, often complex, fund structure. A primary duty here is calculating the fund’s Net Asset Value (NAV)—the official “share price” of the fund at any given time.

This isn’t as simple as checking a stock ticker. It involves valuing illiquid assets, tracking every single fund expense, and keeping the financial records airtight. Administrators also manage the capital accounts for each Limited Partner (LP), ensuring every dollar contributed, distributed, or allocated is tracked with absolute precision. This ledger is the bedrock of all investor reporting.

Investor Services and Communication

Beyond crunching numbers, administrators are the operational face of the fund for its investors. They manage the entire LP journey, from the first subscription document to the final distribution check, making the experience professional and seamless. This is a huge part of maintaining LP confidence and building lasting relationships.

Key investor services typically include:

- Managing Capital Calls: When a GP identifies a new investment, the administrator is the one who formally requests the committed capital from LPs.

- Handling Distributions: They process and wire the profits back to investors after a successful exit.

- LP Reporting: Administrators prepare and send out the detailed financial reports, performance data, and other updates that keep investors in the loop.

- Subscription Processing: They handle the mountain of paperwork and due diligence needed when a new investor joins the fund.

Treasury and Regulatory Compliance

Managing a fund's cash is a job in itself. Administrators provide crucial treasury services, overseeing the fund’s bank accounts, processing wires for investments, and coordinating the flow of capital calls and distributions. They make sure the right amount of cash is in the right place at the right time.

At the same time, they act as the fund’s compliance guardians. This means running rigorous Know Your Customer (KYC) and Anti-Money Laundering (AML) checks on every investor to prevent any illicit financial activity. Keeping up with the constantly shifting global regulatory landscape is a massive part of their value, protecting the fund and its managers from serious legal and financial blowback.

A third-party private equity fund administrator gives investors the benefit of knowing there is independent oversight in the accounting and cash movement processes, which is a major driver of confidence.

To see these principles applied in a specific asset class, you can explore these essential real estate fund administration strategies. It's a great way to understand how the core functions adapt to different investment types.

To really bring it all together, let's look at a breakdown of the core services a PE fund administrator provides. The table below shows how their diverse responsibilities contribute to a fund's overall health and success.

Core Services Offered by PE Fund Administrators

As you can see, their role is comprehensive. They are not just service providers but strategic partners who build the operational foundation that a successful private equity fund needs to thrive.

Why Top Firms Outsource Fund Administration

The private equity world is in the middle of a huge operational shift. More and more firms are realizing that managing their own fund administration in-house is not just inefficient—it’s risky. What used to be the default way of doing things is now under a microscope, thanks to a perfect storm of external pressures and internal limitations.

Let's be honest, handling complex fund accounting, investor communications, and regulatory filings yourself is a massive undertaking. It demands a significant investment in specialized talent and expensive technology. This doesn't just create high fixed costs; it pulls the firm's leadership away from what they do best: sourcing deals and generating returns. As a result, outsourcing to professional private equity fund administrators is quickly becoming the new industry standard.

The Outsourcing Trend is Gaining Serious Momentum

This move toward third-party administration isn't just a gut feeling; the numbers tell a clear and compelling story. While it's true that self-administration is still more common in private equity than in the hedge fund world, that's changing fast.

A landmark industry analysis revealed a stark contrast: while only 8% of hedge fund assets are self-administered, a whopping 62% of private equity fund assets still are. But here's the kicker—that gap is closing. Over just three years, the number of independently administered PE funds shot up at a 22% compound annual growth rate (CAGR). That growth rate absolutely towers over the 11% CAGR for self-administered funds. You can read the full research on private equity administration trends to see just how deep this migration runs.

This isn't a minor adjustment. It's a fundamental change in how the best firms think about their operations, moving from a DIY mindset to a more strategic, partnership-driven model.

What's Driving the Change?

So, why the sudden rush to hand over the back-office keys? A few powerful forces are pushing fund managers to look for outside help. This isn't just about offloading tedious tasks; it's about gaining a competitive advantage, slashing risk, and building a firm that's ready for the future.

- Investors are Demanding More: Today’s Limited Partners (LPs) are sophisticated and expect institutional-grade transparency and reporting. Using an independent administrator adds a layer of credibility and reassures LPs that their reports are being handled with the highest professional standards.

- The Regulatory Maze is Getting Tougher: Trying to keep up with the tangled web of global regulations—from KYC/AML to a dozen different reporting standards—is a full-time job. Administrators live and breathe compliance, protecting firms from costly mistakes and reputational hits.

- Getting Access to Better Tech: Building and maintaining a world-class technology stack is incredibly expensive. Outsourcing gives you immediate access to advanced platforms for accounting, data management, and LP portals, all without the massive upfront cost.

By outsourcing non-investment functions, private equity managers can focus on their core competency—investment management—and potentially improve operational efficiency, reduce costs, and manage risks better.

In short, this strategic move turns a fixed operational cost into a variable one. It gives a firm the agility to scale its back office up or down as needed, without the usual growing pains.

Escaping the Headaches of In-House Administration

Let’s face it, running fund administration internally comes with its own set of chronic problems that can stifle a firm's growth. Finding and keeping top-tier back-office talent is a constant, expensive battle, and when a key person leaves, it can create a huge operational gap.

On top of that, in-house teams can easily become siloed, losing touch with the broader industry best practices that a third-party administrator sees every day across dozens of funds. For firms that are serious about upgrading their operations, exploring professional services designed for private equity can provide a clear roadmap to better efficiency and institutional credibility. Outsourcing is the direct solution to these pain points, offering stability, scalability, and access to a deep bench of specialized expertise you simply can't build overnight.

Understanding Fund Administration Fee Structures

Figuring out what it costs to hire a private equity fund administrator can feel a bit like reading tea leaves. There’s no simple price tag. Instead, the final number is a blend of different pricing models and the unique DNA of your fund. Getting a handle on these moving parts is the first real step to building a partnership that makes sense for your bottom line.

Think of the fee structure not just as a cost, but as a reflection of the work your administrator will be doing. A fund with a simple buy-and-hold strategy is a totally different beast than a VC fund juggling multiple, complex financing rounds every quarter. If you can read a fee proposal with a critical eye, you can make sure the price you pay aligns with the value you get.

Comparing Fund Administration Fee Models

Most proposals you'll see will be built on one of three core models, or maybe a mix of them. Each has its own logic and fits certain types of funds better than others. The trick is finding a structure where your administrator is paid fairly for their work, and your fund gets top-notch service without breaking the bank.

Here’s a look at how these common fee models stack up, giving you a clearer picture of what to expect when you're comparing proposals from potential fund administrators.

Ultimately, no single model is universally "best." The right fit depends entirely on your fund’s strategy, size, and how you prefer to manage your operational budget. A good administrator will walk you through these options to find a structure that works for everyone.

What Drives Your Final Cost?

So, you understand the models. But what actually pushes the final number up or down? Several key factors directly influence the quote you get from an administrator, and they all come down to the amount of work and specialized expertise your fund demands. This is why a fund with the same AUM as yours might get a completely different price.

The complexity of the fund's legal structure, the number of portfolio companies, and the frequency of transactions are the primary cost drivers. A simple structure with few transactions will always be less expensive to administer than a multi-layered master-feeder fund with constant activity.

Let's break down the main things that will move the needle on your bill:

- Fund Complexity: Is your fund a straightforward structure, or does it involve multiple legal entities, cross-border investments, and a tricky waterfall? The more complex it is, the more accounting and administrative muscle is needed.

- Number of Investors: Every Limited Partner (LP) represents more work, from the initial KYC/AML onboarding to ongoing communications, capital calls, and distributions. A fund with 50 LPs is a much lighter lift than one with 250.

- Transaction Volume: If your strategy involves frequent deals, follow-on investments, or exits, expect that to be reflected in the price. High activity means more hands-on accounting and valuation work.

- Reporting Requirements: Do your LPs expect bespoke, highly detailed reports? Custom reporting takes more time and resources to prepare than standard templates, and the fee will reflect that.

The best private equity fund administrators are transparent about their pricing. They'll work with you to build a fee structure that makes sense for the services you actually need. The key is to go into those conversations armed with a clear understanding of these models and drivers, so you can lock in a partnership that truly supports your fund.

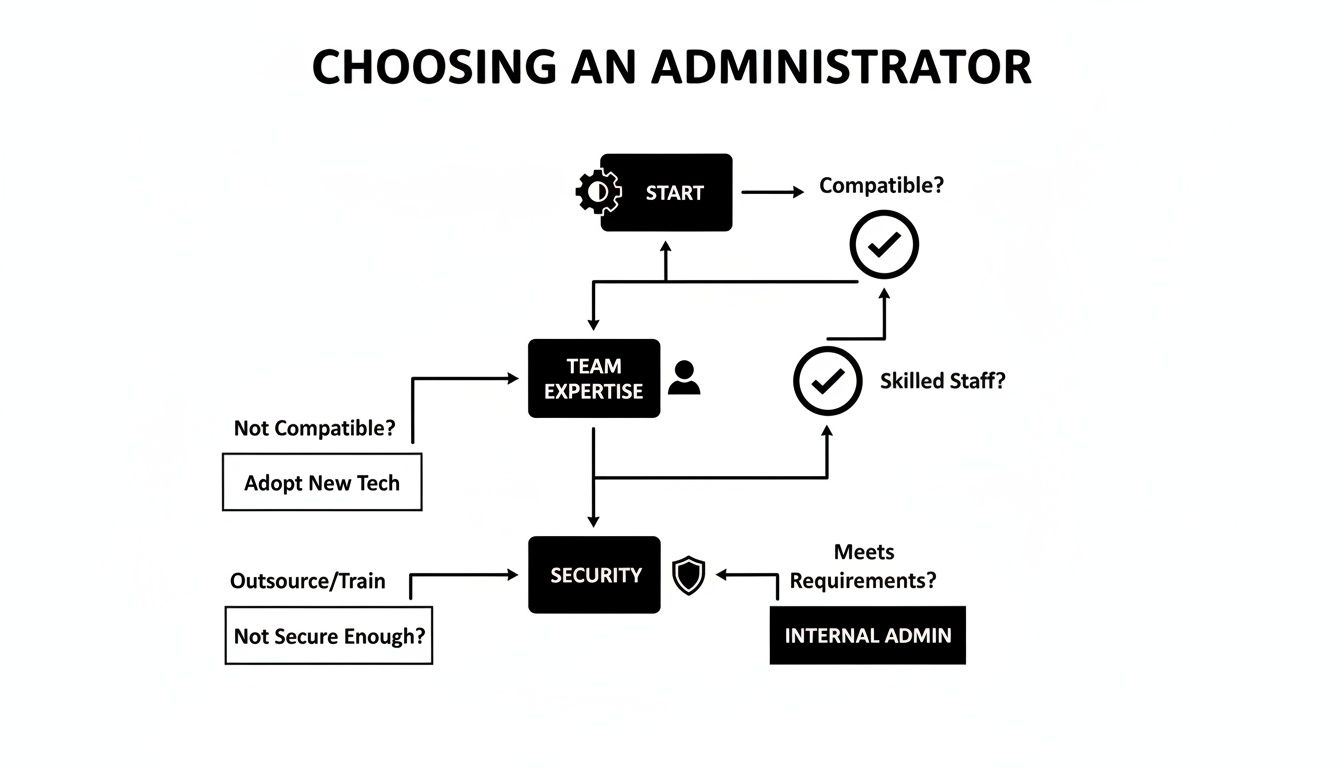

How to Choose the Right Fund Administrator

Picking a private equity fund administrator is one of the most critical decisions you'll make as a fund manager. This isn't just about outsourcing a function; it's about bringing a strategic partner into the fold who will become a direct extension of your team. The right administrator strengthens your operational backbone and bolsters investor confidence. The wrong one can saddle you with years of operational headaches and put your reputation on the line.

Making the right call demands a thorough and structured due diligence process that goes well beyond comparing fee schedules. You need to get under the hood of their technology, vet the experience of their team, and make sure there's a genuine cultural fit. In a market where operational excellence is no longer a "nice-to-have" but a key differentiator, finding this partner is everything.

Evaluate Their Technology and Integration Capabilities

An administrator's technology platform is the heart of their entire operation. A modern, powerful platform isn't negotiable—it directly affects data accuracy, reporting speed, and how efficiently your fund runs. As you kick the tires, treat their platform with the same scrutiny you'd apply to any critical piece of your own infrastructure.

Your main goal here is to find a partner whose tech breaks down data silos, not builds new ones. With global private markets assets under management growing at nearly 20% a year since 2018, the sheer volume of data is staggering. It's no surprise that a recent study found that a whopping 43% of a private markets professional's time is wasted just copying and pasting data between disconnected systems. You can see for yourself how data fragmentation hobbles fund operations and understand why so many firms are demanding a single source of truth.

When you're in the weeds, here's what to focus on:

- Platform Functionality: Don't just watch a slick presentation—demand a full, hands-on demo. Can you get a clean, immediate view of fund performance, capital accounts, and investor data? How quickly can your team get up to speed on the interface?

- Integration Power: How well does their platform play with others? Ask for specific, real-world examples of how they've connected their system to portfolio management tools (like Vestberry), CRMs, or other software you rely on.

- LP Portal Experience: Put yourself in your investors' shoes and take a hard look at their LP portal. Is it intuitive? Is it secure? Does it deliver the kind of on-demand, detailed information that modern LPs now expect as standard?

Assess the Team and Their Strategic Expertise

While great technology is crucial, it’s the people behind the screen who will ultimately define your experience. An administrator’s team needs to be more than just a group of accountants; they should be seasoned specialists who truly get the nuances of your fund's specific strategy. This human element is what separates a reactive vendor from a proactive partner.

The depth of their team's experience is paramount. You need the confidence that comes from knowing the people handling your fund's complex inner workings have been there and done that.

A quality team can feel like an extension of your own office. Tenure of the team, turnover, and culture play an important role in the service level managers receive, so inquire about those items and historical turnover trends.

As you vet potential private equity fund administrators, be sure to dig into their human capital:

- Direct Experience with Your Strategy: Has the team worked extensively with funds like yours? Look for a proven track record matching your fund's size, complexity, and investment focus, whether it's venture capital, buyout, or real estate.

- Access to Senior Leadership: When a complex issue inevitably crops up, how easy is it to get a senior expert on the phone? The last thing you want is to be stuck with a junior contact when the stakes are high.

- Team Stability and Culture: High employee turnover is a massive red flag. Ask directly about team tenure and their philosophy on client service. This will give you a real sense of the organization's stability and whether their culture aligns with yours.

Scrutinize Security Protocols and Client References

In a world of constant cyber threats, rock-solid security isn't just a feature—it's the price of entry. A security breach at your administrator is, for all intents and purposes, a breach of your firm and a violation of your investors' trust. You have to verify that they have institutional-grade security protocols in place to guard sensitive financial and personal data.

Finally, never underestimate the value of talking to their current clients. References give you an unfiltered, real-world view of what it's actually like to work with the administrator. Ask tough questions about their responsiveness, accuracy, and how they handle the unexpected. This on-the-ground feedback is often the most valuable insight you'll get, ensuring you end up with a partner who truly walks the talk.

Boosting Investor Confidence and Fundraising Success

A top-tier fund administrator does more than just balance the books—they can be one of your most powerful assets in fundraising and managing Limited Partner (LP) relationships. In a crowded market, bringing a reputable, independent administrator on board sends a clear message to potential investors: you're serious, professional, and built for institutional-level operations.

This simple decision shifts a back-office function squarely into the realm of competitive advantage. When LPs see that an objective third party is handling critical tasks like accounting, compliance, and reporting, it adds a crucial layer of independent oversight. For sophisticated investors who live and breathe operational due diligence, that assurance can be the deciding factor.

Turning Operations Into a Fundraising Tool

There’s a direct line between solid operations and investor trust. A smooth, professional subscription process sets the right tone from day one. This is where administrators shine, efficiently handling KYC/AML checks, managing paperwork, and answering investor questions without missing a beat. This frees you, the GP, to focus on building relationships instead of getting bogged down in administrative quicksand.

A well-oiled operational machine shows that your fund is managed with precision and care. It’s the kind of confidence-builder that helps get commitments over the line, especially from large institutional investors who scrutinize every detail.

By outsourcing non-investment functions, private equity managers can focus on their core competency—investment management—and potentially improve operational efficiency, reduce costs, and manage risks better.

This shift allows you to actively use your administrator's reputation and proven processes as a tangible part of your fundraising pitch.

Meeting the Demands of a Growing Market

The private equity world is expanding at a dizzying pace, making operational excellence more critical than ever. Just look at the first half of 2025: global PE funds locked down an incredible $424.58 billion across 1,081 funds, already blowing past half of the total raised in all of 2024. This wave of capital from pensions, sovereign wealth funds, and other major players puts immense pressure on a fund’s internal engine. They expect flawless execution on everything from LP reporting to capital calls and distributions. As S&P Global Market Intelligence details, administrators are the bedrock for managing this complexity.

The flowchart below breaks down the key decision points—technology, expertise, and security—you need to weigh when choosing a partner capable of handling this scale.

As the chart shows, the right choice isn't just about one thing. It's a balanced assessment of their tech stack, their team's real-world expertise, and their commitment to ironclad security.

Enhancing the Limited Partner Experience

The value of a great administrator doesn’t stop once the fund is closed. They are absolutely vital for maintaining strong, long-term relationships with your LPs. Their job is to ensure every communication and report is accurate, on-time, and professional. A huge part of this is giving investors easy, self-service access to their own information.

Today's investors expect a high-quality digital experience—it's not a "nice to have," it's a baseline requirement. This is where an administrator's technology, especially their investor portal, can make or break the LP experience. You can see what a modern LP portal should offer to keep investors happy and informed.

Here’s what a superior LP experience looks like in practice:

- On-Demand Access: LPs can log in securely anytime, anywhere to pull capital account statements, check fund performance data, or review legal documents. No more waiting for emails.

- Professional Reporting: Reports are delivered on a consistent schedule in a clean, easy-to-digest format. This reinforces your fund’s commitment to transparency.

- Efficient Communications: Capital call and distribution notices are handled methodically and clearly, which cuts down on errors and headaches for everyone involved.

By delivering this kind of seamless and transparent service, an administrator helps build the lasting trust that turns a one-time LP into a repeat investor for your future funds.

Frequently Asked Questions

When you're running a fund, the idea of bringing on an administrator brings up a lot of questions. Let's walk through some of the most common ones that GPs and fund managers ask as they explore this path.

Think of this as a practical Q&A to clear up the thresholds, roles, and real-world logistics of working with a fund admin.

Key Considerations for GPs

At what fund size does it make sense to hire a third-party administrator?

There's no single magic number, but the conversation usually gets serious once a fund's assets under management (AUM) start creeping into the $50 million to $100 million range.

Why then? At that point, the sheer volume of work—from LP reporting and capital calls to navigating dense regulatory filings—starts to overwhelm a small internal team. It's not just about the hours; it's about the risk of dropping the ball when you're stretched too thin.

What is the difference between a fund administrator and a fund accountant?

It’s easy to mix these up, but the difference is huge. A fund accountant is a specialist focused squarely on the numbers. Their world revolves around calculating the Net Asset Value (NAV), tracking portfolio investments, and preparing the fund's financial statements.

A private equity fund administrator, on the other hand, provides a much broader, more holistic service. They handle all the fund accounting, but then they layer on investor services (like onboarding and fielding LP questions), treasury management, compliance oversight, and general regulatory support. In short, they manage your fund’s entire back-office operation.

By outsourcing non-investment functions, private equity managers can focus on their core competency—investment management—and potentially improve operational efficiency, reduce costs, and manage risks better.

One is a specific accounting role; the other is a full-blown operational partnership.

Logistical and Practical Queries

Can we switch fund administrators mid-fund life?

The short answer is yes, you can. But it’s a massive project and definitely not something you should take lightly.

Think about it: you're migrating years of historical data, re-onboarding every single LP, and coordinating a handoff between the old and new providers where nothing can get lost in translation. It’s a delicate, high-stakes process.

Because it can be so disruptive for your team and your investors, most GPs only make a switch if they're dealing with major service failures or if their current admin just can’t provide a critical technology upgrade. If you do decide to make a change, a flawless execution plan is non-negotiable to keep your LPs happy.

Ready to transform your fragmented data into actionable portfolio intelligence? Vestberry provides a single source of truth for VCs and PEs, replacing manual work with powerful analytics and automated LP reporting. See how you can make faster, data-backed decisions.