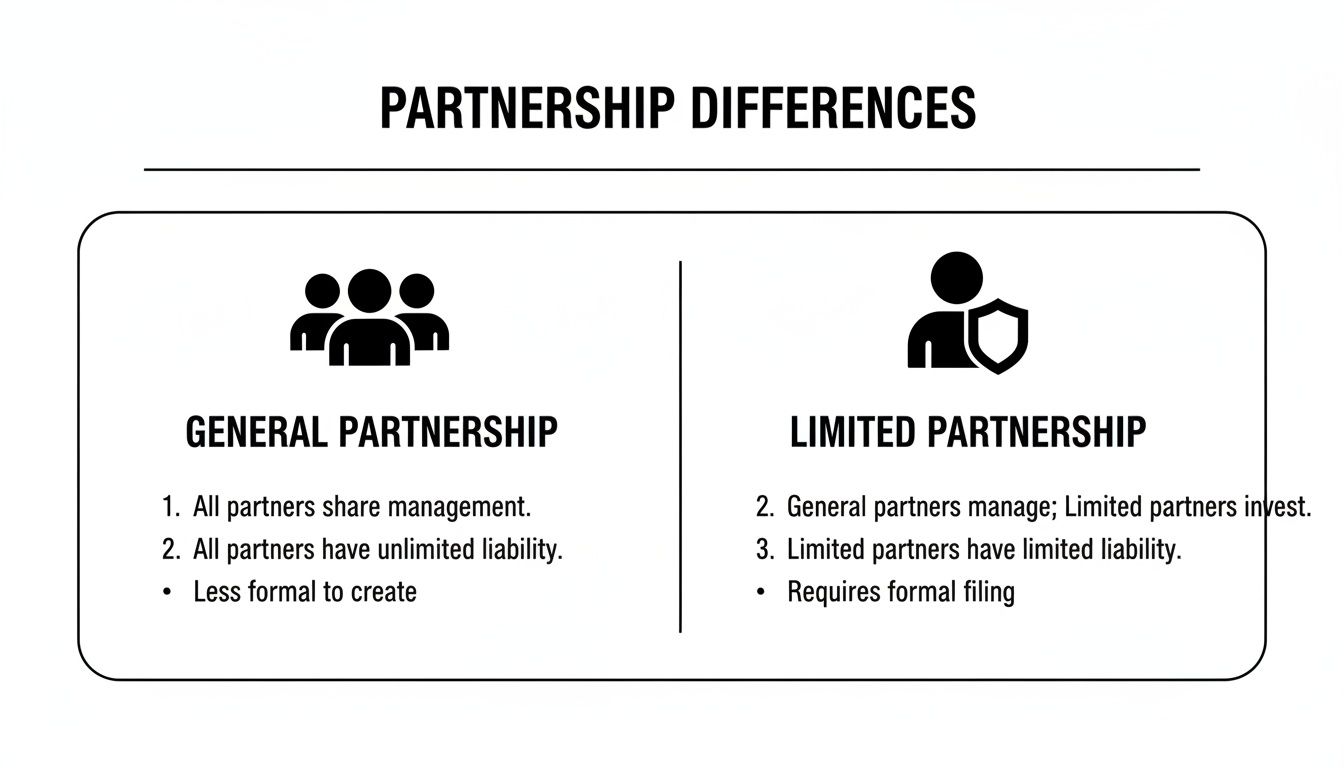

The real difference between a general and limited partnership boils down to two things: liability and management. In a general partnership, every partner is in it together, sharing equal say in management and, critically, unlimited personal liability for the business's debts.

A limited partnership, on the other hand, is a different beast entirely. It's purpose-built for investment, creating a clear split between the active managers and the passive investors.

Decoding Partnership Structures for Venture Capital

When you look at the world of venture capital (VC) and private equity (PE), the limited partnership isn't just an option—it's the industry standard. This structure is the engine of the entire private investment ecosystem, perfectly designed to align the goals of hands-on fund managers with the institutions and individuals who provide the capital.

If you're involved in fund management or deal with investor relations, grasping this distinction is non-negotiable. The legal separation of roles is what allows VCs to pool massive amounts of capital while defining exactly who is responsible for what and how much risk each party takes on.

Here’s a quick breakdown of the key players:

- General Partners (GPs): Think of these as the fund managers. They’re the ones on the ground sourcing deals, doing the due diligence, making the tough investment calls, and actively working with portfolio companies. In return for this control, they accept unlimited liability for the fund's debts and obligations.

- Limited Partners (LPs): These are the investors—the pension funds, university endowments, and family offices that write the checks. Their role is intentionally passive. The critical trade-off is that their financial risk is capped at the amount they invested, which keeps their other assets safe.

This setup is what makes the high-stakes game of venture investing possible in the first place.

This visual gives a great high-level overview of how these two structures fundamentally differ.

As you can see, that liability shield is the single biggest reason passive investors are drawn to the limited partnership model. Getting these foundational elements right from the start is crucial, and understanding how to structure a business partnership effectively offers essential insights into the legal mechanics that empower managers and attract serious capital.

Key Differences At a Glance General vs Limited Partnership

For a quick side-by-side comparison, this table breaks down the most important distinctions between the two partnership types.

This table really highlights how the limited partnership is specifically engineered for investment scenarios where capital providers need protection from day-to-day operational risks.

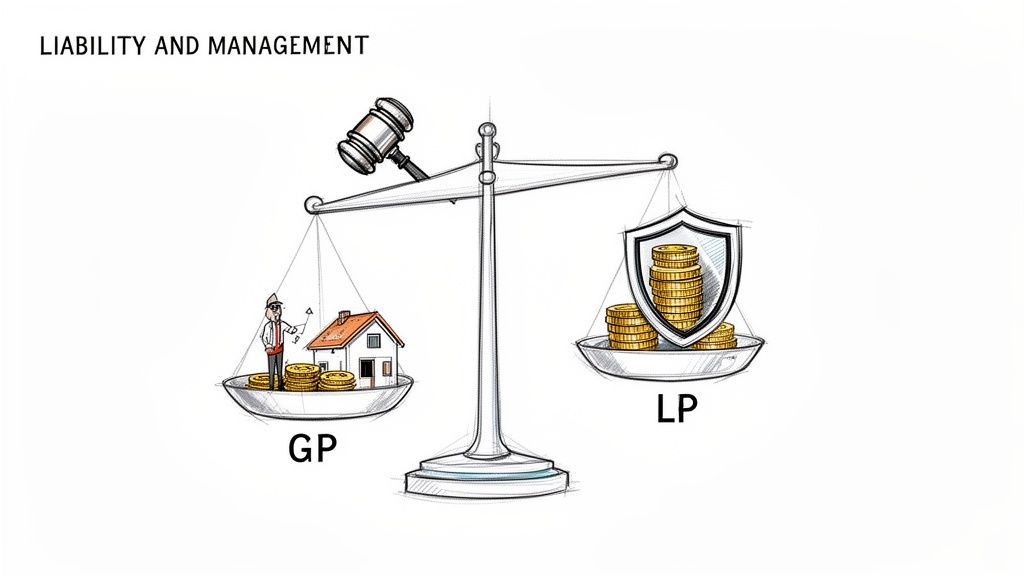

A Look at Liability and Management Control in Fund Structures

At the heart of any venture capital or private equity fund, the difference between a general and a limited partnership comes down to two things: risk and authority. How these two elements are balanced isn't just a legal formality; it's the very foundation that allows institutional investors to commit capital in the first place. Liability and management control are two sides of the same coin, defining the roles, responsibilities, and financial exposure for everyone involved.

Why Liability Protection is Non-Negotiable

Imagine a general partnership as a shared, bottomless pit of liability. Every partner is jointly and severally liable for all business debts. What that means in practice is that a creditor could go after any single partner for the entire amount of a debt, regardless of how small that partner's individual stake might be.

This setup is an immediate deal-breaker for any serious investment fund. No sophisticated investor—from a pension fund to a wealthy individual—would ever agree to put their entire personal net worth on the line because a portfolio company went south or the fund faced a lawsuit. The personal financial risk is simply too great.

This is precisely where the limited partnership (LP) model comes in. It creates a critical legal shield for its investors, the Limited Partners.

The single most important feature of a limited partnership is that an LP’s liability is legally capped at the amount of their capital contribution. If an LP commits $5 million to a fund, that is the absolute maximum they can lose. Their personal assets remain untouchable.

This protection is the bedrock of the entire private equity and venture capital world. It’s what allows fund managers to pool capital from passive investors who trust them to execute a strategy without fearing personal financial ruin. For the General Partners (GPs), however, the story is quite different—they take on unlimited personal liability as the trade-off for having control.

Tying Management Authority to Liability Exposure

The way management control is distributed directly mirrors the liability structure. The legal logic is simple: if you have the power to make decisions that create risk, you should be the one to bear the ultimate responsibility for that risk.

General Partnership Control

- Shared and Equal: By default, every partner gets an equal say in managing the business and can make decisions that bind everyone else. One partner’s handshake can legally obligate all the others, even if they knew nothing about it.

- Hands-On by Design: This structure is built for partners who are all active participants, involved in the day-to-day work and strategic planning.

Limited Partnership Control

- Centralized in the GP: All management power is placed exclusively in the hands of the General Partner(s). LPs are legally walled off from participating in the daily management of the fund.

- The Passive Investor Role: An LP’s job is to provide the capital, period. If an LP gets too involved and starts making management decisions, they risk losing their limited liability protection and being treated like a GP in court.

This clear separation of duties is crucial. The GP has a fiduciary duty to act in the best interests of the LPs, while the LPs provide the fuel for the fund's investments, trusting the GP's expertise. Organizations like the Institutional Limited Partners Association (ILPA) offer guidelines to help govern this relationship, promoting transparency and alignment. As funds scale, managing these complex relationships and reporting requirements demands robust systems. Becoming a data-driven fund is key to meeting these obligations, a topic you can explore further by learning how to drive digital adoption and become a data-driven-pe-vc-fund.

While the LP model is the standard for investment funds, it's not the only partnership structure out there. For a different perspective on liability and governance, it's worth exploring the Limited Liability Partnership (LLP) structure, which is common among professional firms like law and accounting practices and provides liability protection for all partners. Comparing these structures really highlights why the specific GP/LP model is so perfectly suited for the world of institutional investing.

Understanding Capital Contributions and Tax Implications

The way money moves through a general partnership versus a limited partnership couldn't be more different, especially when you step into the world of venture capital and private equity. While they both share a foundational tax treatment, how they handle capital reflects their distinct roles. A general partnership's finances are pretty straightforward—ideal for a hands-on operational business. An investment fund's limited partnership, on the other hand, is a precisely engineered system of capital calls, fees, and distributions.

Financial Flows in a General Partnership

In a standard general partnership, partners typically contribute capital right at the start. Everyone pools their resources—whether it's cash, property, or even sweat equity—to get the business off the ground. This initial pot of money is the financial bedrock of the whole operation.

From there, profits and losses are split based on the partnership agreement. If you don't have one, state law usually steps in and mandates an equal split, regardless of who put in more. It’s a simple, direct model that works perfectly for businesses where every partner has a hand in running things.

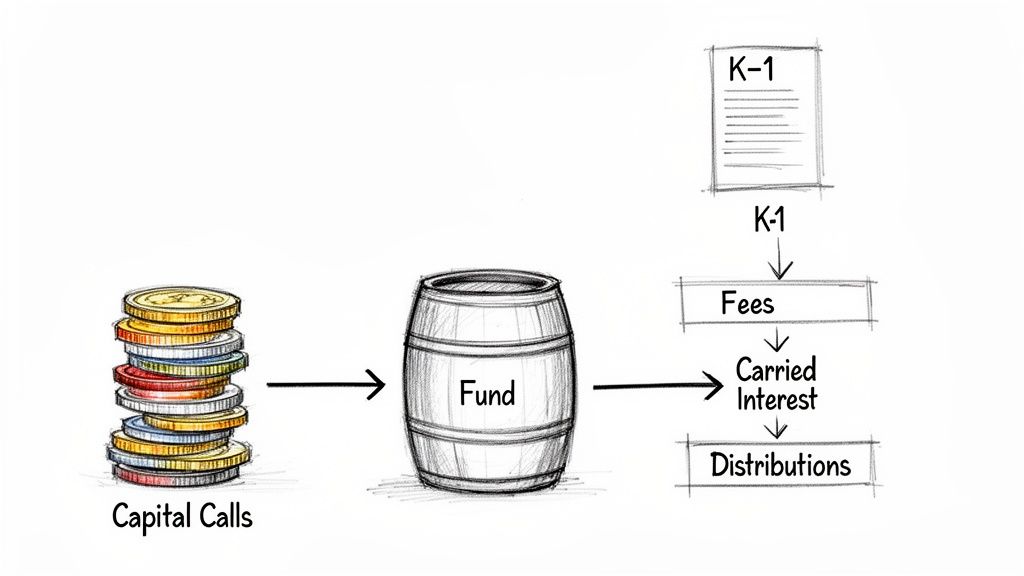

The Sophisticated Capital Structure of a Limited Partnership

The limited partnership model, which is the gold standard in VC and PE, is a whole different ballgame. Limited Partners don't just write one big check. Instead, they commit a certain amount of capital, and the General Partner makes capital calls to draw down that money over time as investment opportunities pop up.

This "just-in-time" funding approach is incredibly efficient, letting the fund deploy capital exactly when it's needed. It also brings a few unique financial mechanics into play:

- Management Fees: To keep the lights on and cover operational costs, GPs charge an annual fee, usually between 1.5% to 2.5% of the committed capital. This pays for the GP's work in managing the fund, sourcing deals, and supporting portfolio companies.

- Carried Interest: This is the big one. "Carry" is the GP's slice of the fund's profits, typically 20%, but it only kicks in after LPs get their initial investment back, plus a preferred return (the "hurdle rate"). It’s the primary incentive for fund managers to knock it out of the park.

- Distribution Waterfall: This is the playbook for how profits are paid out. It’s a specific, sequential process ensuring that money flows back in the right order—LPs get their principal back first, then their preferred return, and only then does the GP start seeing carried interest.

This entire structure is designed to align everyone's interests. It rewards the GP for generating great returns while making sure the investors who provided the capital are first in line to get paid.

The Unifying Principle of Pass-Through Taxation

For all their differences, both partnership types share one powerful tax feature: they are pass-through entities. This means the partnership itself doesn't pay income tax. Instead, all profits and losses are "passed through" directly to the partners, who report them on their personal tax returns.

This is a huge advantage over C-corporations, which get hit with double taxation—once at the corporate level and again when profits are paid to shareholders. IRS data from 2023 shows just how dominant these structures are. While general partnerships are fading, limited partnerships are a powerhouse, with 10.3 million partners and $689.1 billion in pass-through income. You can dig deeper into these figures in the latest IRS partnership statistics.

For fund managers, the pass-through structure creates one of the biggest administrative headaches: generating and distributing Schedule K-1 forms to every single LP. Each K-1 breaks down an investor's share of the fund's income, deductions, and credits. Getting this right is non-negotiable for tax compliance, which is why modern portfolio intelligence platforms have become so crucial for automating K-1s and ensuring accurate reporting for hundreds of investors.

Key Tax Considerations for Partners

In a general partnership, every partner is usually considered an active participant. That means they have to pay self-employment taxes—contributions to Social Security and Medicare—on their share of the partnership’s earnings.

The situation is more nuanced in a limited partnership. General Partners pay self-employment tax on their management fees and their slice of the business income. But Limited Partners, as passive investors, generally don't have to pay self-employment tax on their share of the fund's profits. This distinction sharpens the line between the active manager and the passive capital provider, making the limited partnership an even more tax-efficient vehicle for investors.

9. Fund Formation, Governance, and Exit Mechanics

For anyone launching a new fund, getting the mechanics of formation, governance, and dissolution right isn't just a legal hoop to jump through—it's the very foundation of your fund's operational success and your relationship with investors. Your choice between a general and limited partnership will shape this entire lifecycle.

A general partnership can be as simple as a handshake agreement. A venture capital fund, on the other hand, is almost always a limited partnership, which demands a meticulous, document-heavy formation process built to protect everyone involved.

The legal bedrock of a VC fund is a specific set of documents that formalize the relationship between you, the General Partner (GP), and your investors, the Limited Partners (LPs).

- The Limited Partnership Agreement (LPA): Think of this as the fund's constitution. It's a heavily negotiated contract that spells out everything—the investment strategy, fund term, management fees, carried interest, and the precise rules for calling capital and distributing profits.

- The Private Placement Memorandum (PPM): This is your fund’s business plan and disclosure document, rolled into one. The PPM gives prospective LPs all the information they need to make a smart investment decision, covering your team, strategy, market analysis, and, crucially, the risk factors.

- Subscription Documents: This is the actual paperwork an LP signs to commit capital. It locks in their investment amount and legally binds them to the terms laid out in the LPA.

Establishing Governance and Reporting Obligations

Once the fund is live, the LPA acts as the rulebook for governance, with a major focus on the GP's duty to report to the LPs. This is a massive departure from a general partnership, where every partner is typically in the driver's seat. In the LP structure, investors trade their management rights for liability protection, which makes transparent and regular communication from the GP absolutely non-negotiable.

These reporting duties aren't just good practice; they're contractual obligations. At a minimum, you'll be responsible for:

- Quarterly Reports: Detailed updates on fund performance, new deals, portfolio company progress, and financial statements.

- Annual Meetings: A chance for the GP to give a comprehensive overview of the fund's year and for LPs to ask questions face-to-face.

- Capital Account Statements: Regular snapshots showing each LP's contributions, distributions, and what's left of their commitment.

Strong LP reporting is the glue that holds the GP-LP relationship together. It goes beyond just checking a box; it builds trust and shows you have a firm handle on the portfolio. That means having the portfolio intelligence to accurately track metrics like IRR, TVPI, and DPI.

Modern fund managers rely on sophisticated platforms to handle these reporting demands. If you want to stand out, it's worth learning more about improving LP reporting in venture capital to keep your investors happy.

The clear preference for the LP structure shows up in long-term economic data. Looking at trends from 2012 to 2023, the shift is undeniable, driven largely by the liability shield LPs offer. In the 2021 tax year, general partnerships—with their unlimited personal liability—made up just 12.6% of all partnerships, a steady decline from their pre-2002 dominance. In stark contrast, limited partnerships managed $1.4 trillion in pass-through income across 10.4 million partners, cementing their role as the primary vehicle for capital formation in private markets.

Managing Transferability and Fund Dissolution

The end of a fund's life—the exit—is another area where these two structures couldn't be more different. In a general partnership, one partner leaving can throw the whole business into chaos, potentially even forcing a dissolution if the partnership agreement doesn't have a plan for it.

The process in a limited partnership is far more orderly and predictable.

LP interests are intentionally illiquid. An investor can't just sell their stake on a whim. Any transfer, which usually happens in a secondary sale to another institutional investor, requires the GP's explicit approval. This control is critical for preventing unwanted partners from joining the fund and maintaining stability.

Finally, when the fund's term is up (typically 10-12 years), the GP starts the wind-down process. This means liquidating the last of the assets, settling any debts, and making final payouts to the LPs based on the distribution waterfall defined in the LPA. Once all the cash is out and the final reports are sent, the GP files a certificate of cancellation with the state, and the limited partnership is officially dissolved.

VC Fund Structuring Checklist LP vs GP Considerations

For fund managers navigating these choices, a clear checklist can help crystallize the decision-making process. The table below outlines the key considerations when comparing a general partnership approach to the industry-standard limited partnership model for a venture capital fund.

This checklist underscores why the limited partnership has become the default structure for venture capital. It provides the necessary liability protection to attract investors and the centralized management control for the GP to effectively deploy capital and run the fund.

Why Limited Partnerships Dominate the Venture Capital Industry

After laying out the differences between general and limited partnerships, one thing becomes crystal clear. The limited partnership isn't just a popular choice for venture capital and private equity—it's the very foundation that makes the industry work. It was a strategic innovation designed to solve one massive problem: how to pool huge amounts of passive capital under the control of specialized, active managers.

This structure brilliantly aligns the goals of everyone involved. On one side, you have Limited Partners (LPs)—often large institutions like pension funds or university endowments. They need to put capital to work in high-growth opportunities, but they can't get bogged down in day-to-day operations or expose themselves to unlimited risk.

On the other side are the General Partners (GPs), the fund managers. They need the freedom to execute a risky investment strategy and a clear path to significant upside. The limited partnership is the only model that elegantly serves both masters.

The Engine of High-Risk Investment

The dominance of the limited partnership structure is nothing new; its power to attract capital is deeply rooted in history. Research on 19th-century New York partnerships, from 1822 to 1853, shows that limited partnerships were already punching above their weight. While only 773 limited partnerships were formed, by 1853 they had attracted over $6 million in capital from limited partners, capturing a huge share of partnership wealth and setting the stage for modern fund dynamics. For a deeper dive into this history, check out the full research on 19th-century partnership dynamics.

This historical trend points to a fundamental truth that holds just as strong today. When investors are shielded from unlimited liability, they're far more willing to write big checks for high-risk, high-reward ventures. A general partnership, where every partner is on the hook for everything, is a complete non-starter. No institutional investor would ever sign up for a deal that puts its entire endowment at risk.

The real genius of the limited partnership is how it separates liability from capital. It builds a legal firewall between the passive investors (LPs) and the fund’s debts and operational risks, capping their potential loss at the exact amount they invested. This protection is the absolute, non-negotiable price of entry for raising a professional investment fund.

Built for Scalability and Governance

Beyond just protecting investors, the limited partnership provides a clear and robust governance framework that's essential for managing a fund over its entire lifecycle. The Limited Partnership Agreement (LPA) is the rulebook. It defines everything from capital calls and management fees to reporting duties and how profits are split.

This formal structure is absolutely critical for maintaining compliance and building trust with investors. It legally establishes the GP’s fiduciary duty and requires transparent reporting—both essential for managing the complex web of stakeholders in any fund. For fund managers, this clarity helps them make data-driven decisions and ensures every action is aligned with the LPA. Given the vast ecosystem of investors, which you can learn more about in our guide to over 6000 limited partners investing in VC and PE, it's easy to see why such a strong framework is required.

At the end of the day, a general partnership is built for a small, hands-on business where every partner is in the trenches together. The limited partnership, by contrast, is a pure investment vehicle. Its unique mix of investor protection, centralized management, and scalable governance makes it the undisputed—and really, the only—viable choice for the venture capital industry.

Frequently Asked Questions

Even when you've got the basics down, real-world situations always bring up new questions for fund managers and investors. Here are some straightforward answers to the common questions we hear when people are sorting through fund structures.

Can a Limited Partner Lose More Than Their Investment?

No, they can't. The bedrock principle of a limited partnership is that an LP’s potential loss is capped at the exact amount of capital they agreed to invest. This creates a crucial legal barrier, protecting their personal assets from any of the fund's debts or legal troubles.

That protection isn't absolute, though. It hinges on the LP staying completely passive. If a limited partner starts getting involved in the day-to-day management of the fund, they risk being reclassified as a general partner in the eyes of the law. That would shatter their liability shield and expose them to unlimited personal risk for the fund's obligations.

What Is the Role of the Limited Partnership Agreement?

Think of the Limited Partnership Agreement (LPA) as the constitution for the fund. It's the binding legal contract that maps out the entire relationship between the General Partner (GP) and every single Limited Partner (LP), defining all rights and duties.

The LPA is the fund's single source of truth. It governs everything—investment strategy, management fees, how and when capital is called, the waterfall for distributions, reporting standards, and the fund's lifespan. It's a deeply negotiated document that sets the ground rules for the fund's entire journey, from day one to dissolution.

Why Would Anyone Choose a General Partnership Structure?

For a professional investment fund? They wouldn't. A general partnership is almost never used in this context because the personal liability risk for every partner is just too high. Its use in modern business is incredibly narrow.

So where does it fit? It can be a simple, quick option for very small, hands-on businesses where all partners are actively running the show and have a high degree of trust. Imagine a small family-owned consulting firm or a local professional practice.

The main draws are its simplicity and low setup costs—it often requires no formal state registration and, by default, gives everyone equal say in management. The fundamental difference between a general and limited partnership really comes down to this trade-off: simplicity versus protection. For any serious investment vehicle, that protection is non-negotiable.

At Vestberry, we know that managing the intricate details of a limited partnership takes more than a solid legal agreement—it requires powerful portfolio intelligence. Our platform turns scattered fund data into clear, actionable insights, helping you automate LP reporting, track performance with precision, and make faster, data-backed decisions. Learn how Vestberry can support your fund.